Why Are Lightweight and High-Strength Aluminum Components Driving the Market Toward USD 756 Million by 2034?

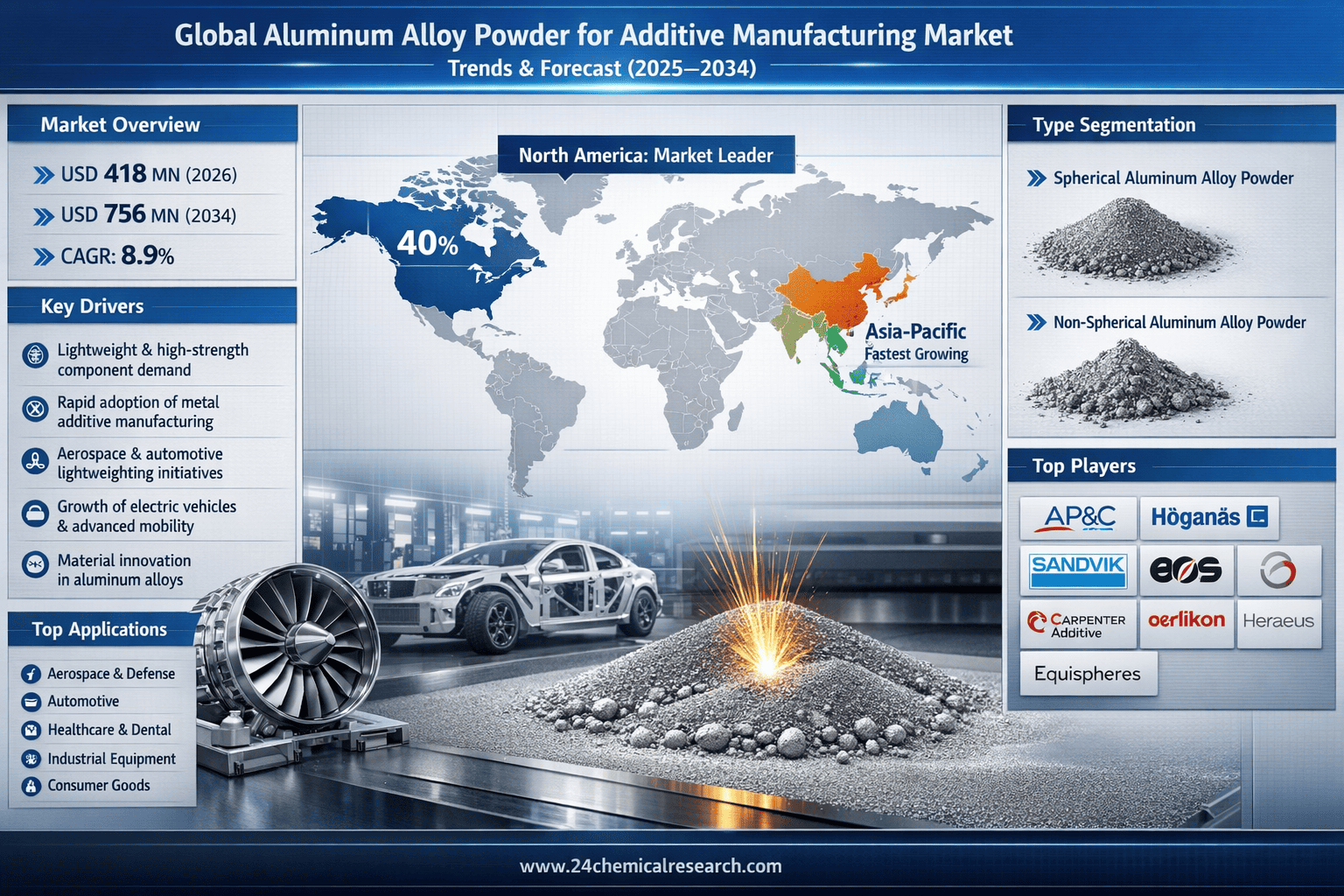

According to 24Chemical Research, Global aluminum alloy powder for additive manufacturing market was valued at USD 418 million in 2026 and is projected to reach USD 756 million by 2034, exhibiting a remarkable CAGR of 8.9% during the forecast period.

Aluminum alloy powder, a precision-engineered metallic feedstock, has evolved from a niche material into a fundamental enabler of industrial additive manufacturing. Composed primarily of aluminum blended with elements like silicon, magnesium, and titanium, these powders are characterized by their spherical morphology, controlled particle size distribution (typically 15-150 micrometers), and exceptional chemical purity. These attributes ensure optimal flowability, layer uniformity, and sintering behavior in powder bed fusion systems. Unlike conventional aluminum forms, these specialized powders facilitate the creation of complex, lightweight, and high-strength components that are revolutionizing product design and manufacturing across critical industries.

Get Full Report Here: https://www.24chemicalresearch.com/reports/300007/aluminum-alloy-powder-for-additive-market

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities.

Powerful Market Drivers Propelling Expansion

-

Revolutionizing Aerospace and Automotive Lightweighting: The integration of aluminum alloy powders into additive manufacturing represents the most significant growth vector, driven by the insatiable demand for lightweighting in transportation. The global aerospace and automotive industries, with a combined value exceeding $4 trillion, are in a perpetual quest for materials that reduce weight without compromising structural integrity. Aluminum AM components enable weight reductions of 30-50% compared to traditionally manufactured parts, a critical advancement for improving fuel efficiency in aircraft and extending the range of electric vehicles. This driver is particularly potent as the aerospace sector increasingly specifies certified AM parts for critical applications, moving beyond prototypes into series production.

-

Technological Advancements in Powder Production and Processing: The additive manufacturing sector is experiencing a renaissance fueled by continuous improvements in both powder production and printing technologies. Advanced gas and plasma atomization techniques now produce powders with near-perfect sphericity, controlled particle size distribution, and oxygen content below 0.15%. Concurrently, advancements in laser powder bed fusion systems have enhanced processing parameters for aluminum alloys, reducing defects like porosity and cracking while improving mechanical properties. These synergistic developments have increased material utilization rates to 95-98% in optimized systems, making AM increasingly competitive with subtractive manufacturing for high-value components.

-

Material Science Innovations in Alloy Development: The materials science field is being transformed by the development of specialized aluminum alloys tailored for additive manufacturing. New scandium-modified aluminum alloys and aluminum matrix composites offer yield strengths exceeding 500 MPa, rivaling some titanium alloys at a fraction of the cost. When incorporated into AM processes, these advanced materials can enhance tensile strength by 40-60% and improve thermal stability by 50-100°C compared to conventional aluminum alloys. These dramatic improvements are driving rapid adoption in demanding sectors like defense, space exploration, and high-performance automotive, where the premium for enhanced performance justifies the material cost.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/300007/aluminum-alloy-powder-for-additive-market

Significant Market Restraints Challenging Adoption

Despite its promise, the market faces hurdles that must be overcome to achieve universal adoption.

-

High Production Costs and Economic Barriers: The sophisticated atomization methods required to produce high-quality aluminum powder, particularly gas and plasma atomization, involve specialized equipment and controlled environments that elevate manufacturing costs by 25-45% above conventional aluminum production. Furthermore, the industrial-grade additive manufacturing systems required to process these powders represent capital investments of $500,000 to $2 million, creating significant economic barriers for small and medium-sized enterprises. The total cost of ownership for metal AM, including powder, equipment depreciation, and operational expenses, remains 3-5 times higher than traditional manufacturing for many applications, posing a substantial barrier for cost-sensitive industries.

-

Regulatory and Standardization Challenges: In highly regulated sectors like aerospace and medical devices, the path to certification for additively manufactured components is complex and time-consuming. Current qualification processes for new materials and processes can extend from 18 to 36 months in major markets, requiring extensive testing and documentation. The lack of universal standards for powder quality, particularly for emerging alloy compositions, creates uncertainty for manufacturers. Regulatory bodies are still developing specific frameworks for AM components, and this transitional period creates additional compliance costs and delays that can discourage investment in new AM applications.

Critical Market Challenges Requiring Innovation

The transition from laboratory success to industrial-scale manufacturing presents its own set of technical and supply chain challenges. Maintaining powder consistency at production volumes exceeding 1,000 kg per month is difficult, with current processes achieving only 80-85% yield of specification-grade material. Furthermore, ensuring powder recyclability and consistency over multiple reuse cycles remains problematic, with some alloys showing property degradation after 5-7 build cycles. These technical hurdles necessitate substantial R&D investments, often consuming 12-18% of revenue for material producers, creating a high barrier to entry for new market participants.

Additionally, the market contends with supply chain complexities particular to reactive metal powders. Aluminum powders require specialized handling under inert atmospheres to prevent oxidation and explosion risks, increasing transportation costs by 8-12% compared to conventional materials. The infrastructure for recycling and reprocessing used aluminum powder is still developing, with only 30-40% of the market currently offering closed-loop material management systems. These logistical challenges create economic uncertainty for potential large-scale adopters considering AM for volume production.

Vast Market Opportunities on the Horizon

-

Healthcare and Medical Device Innovation: Aluminum alloy powders represent a significant opportunity in the medical device sector, particularly for non-implantable applications requiring lightweight, complex geometries. Surgical instruments, diagnostic equipment components, and external orthopedic devices manufactured through AM offer weight reductions of 40-60% compared to stainless steel equivalents. The global medical device market, projected to reach $600 billion by 2030, presents a substantial opportunity for AM aluminum applications. Recent developments in anodized and coated aluminum medical components have demonstrated compatibility with sterilization protocols, opening new possibilities for single-use surgical instruments that combine lightness with cost-effectiveness.

-

Sustainable Manufacturing and Circular Economy Initiatives: Additive manufacturing with aluminum powders aligns perfectly with growing corporate sustainability goals through material efficiency and waste reduction. AM processes typically use 90-95% of input material compared to 10-20% in traditional machining, representing a dramatic reduction in waste. Furthermore, the ability to produce lightweight components contributes to energy savings during product use, particularly in transportation applications. The development of recycled aluminum powders and closed-loop powder management systems enables a circular economy approach that could reduce the carbon footprint of aluminum components by 30-50% compared to conventional manufacturing.

-

Digital Inventory and Distributed Manufacturing: The market is witnessing the emergence of digital inventory models where components are manufactured on-demand rather than stored physically. This trend is particularly valuable for legacy parts in aerospace, defense, and industrial equipment, where aluminum AM can produce replacement components without maintaining expensive physical inventories or retooling for low-volume production. The ability to manufacture components locally using digital files reduces shipping costs and lead times while increasing supply chain resilience. Early adopters in the aerospace MRO (Maintenance, Repair, and Overhaul) sector report inventory cost reductions of 40-60% while improving aircraft availability through faster part production.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into Spherical Aluminum Alloy Powder and Non-spherical Aluminum Alloy Powder. Spherical Aluminum Alloy Powder dominates the market, favored for its superior flow characteristics, high packing density, and consistent layer deposition in powder bed fusion processes. The spherical morphology ensures minimal voids and uniform melting characteristics, leading to components with enhanced mechanical properties and surface finish. This form is essential for high-performance applications in aerospace, medical, and automotive sectors where precision and reliability are paramount. Non-spherical powders are typically used for less demanding applications or alternative AM technologies where flowability is less critical.

By Application:

Application segments include Aerospace and Defense, Automotive, Healthcare and Dental, Industrial Equipment, and Consumer Goods. The Aerospace and Defense segment currently dominates, driven by the critical need for weight reduction in aircraft and spacecraft without compromising strength or safety. However, the Automotive and Healthcare segments are expected to exhibit the highest growth rates in the coming years as these industries increasingly adopt additive manufacturing for both prototyping and production applications.

By End-User Industry:

The end-user landscape includes OEMs, Tier 1 Suppliers, AM Service Bureaus, and Research Institutions. The OEM segment accounts for the major share, particularly in aerospace and automotive, where companies are integrating AM into their production processes for specific high-value components. The service bureau segment is rapidly emerging as a key growth area, providing manufacturing capacity and expertise to companies that haven't yet invested in their own AM capabilities.

Download FREE极 Sample Report: https://www.24chemicalresearch.com/download-sample/300007/aluminum-alloy-powder-for-additive-market

Competitive Landscape:

The global aluminum alloy powder for additive manufacturing market is semi-consolidated and characterized by intense competition and rapid innovation. The top three companies—AP&C (Canada), Höganäs (Sweden), and Sandvik (Sweden)—collectively command approximately 50-55% of the market share as of 2025. Their dominance is underpinned by extensive IP portfolios, advanced production capabilities, and established global distribution networks.

List of Key Aluminum Alloy Powder for Additive Manufacturing Companies Profiled:

-

AP&C (Canada)

-

Höganäs (Sweden)

-

Sandvik (Sweden)

-

EOS GmbH (Germany)

-

Carpenter Additive (United States)

-

Oerlikon (Switzerland)

-

Heraeus (Germany)

-

Equispheres (Canada)

-

Valimet (United States)

-

CNPC POWDER (China)

-

Elementum 3D (United States)

-

AECC BIAM (China)

The competitive strategy is overwhelmingly focused on R&D to enhance product quality and reduce costs, alongside forming strategic vertical partnerships with end-user companies to co-develop and validate new applications, thereby securing future demand.

Regional Analysis: A Global Footprint with Distinct Leaders

-

North America: Is the technological leader, holding a 40% share of the global market. This dominance is fueled by massive R&D investments, a robust additive manufacturing ecosystem, and strong demand from its world-leading aerospace, defense, and medical sectors. The United States is the primary engine of growth in the region, with Canada emerging as a significant hub for advanced powder production technology.

-

Europe & Asia-Pacific: Together, they form a powerful secondary bloc, accounting for 55% of the market. Europe's strength is driven by strong aerospace and automotive industries and significant government support for advanced manufacturing initiatives. The Asia-Pacific region, led by China, Japan, and South Korea, is experiencing rapid growth driven by massive investments in industrial modernization and the establishment of domestic additive manufacturing capabilities across multiple sectors.

-

Rest of World: These regions represent the emerging frontier of the aluminum alloy powder market. While currently smaller in scale, they present significant long-term growth opportunities driven by increasing industrialization, investments in advanced manufacturing technologies, and growing adoption of additive manufacturing across various sectors.

Get Full Report Here: https://www.24chemicalresearch.com/reports/300007/aluminum-alloy极-powder-for-additive-market

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/300007/aluminum-alloy-powder-for-additive-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies,极 and competitive landscapes.

-

Plant-level capacity tracking

-

极Real-time price monitoring

-

Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/