Why Is Global Long-Fiber Thermoplastics Market Expected to Grow at a 3.10% CAGR Through 2034?

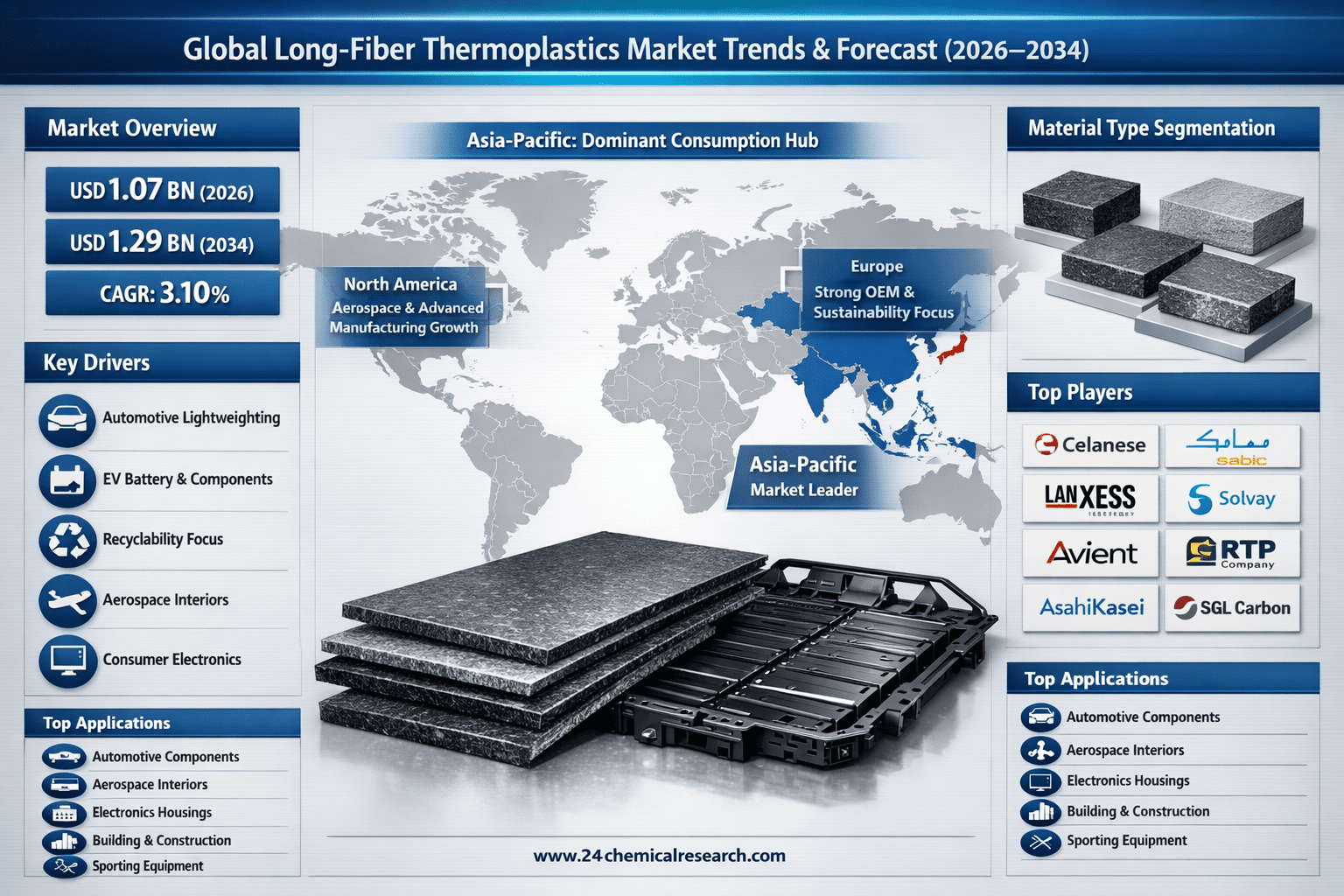

According to 24Chemical Research, Global Long-Fiber Thermoplastics (LFT) Market was valued at USD 1071.00 million in 2026 and is projected to reach USD 1286.30 million by 2034, exhibiting a CAGR of 3.10% during the forecast period.

Long-Fiber Thermoplastics (LFT) represent a class of advanced composite materials where long reinforcing fibers, typically glass or carbon, are integrated into a thermoplastic polymer matrix. These materials have successfully transitioned from niche applications to become essential components in the drive for lightweighting across major industries. Their superior mechanical properties—including high strength-to-weight ratios, excellent impact resistance, and exceptional durability—are central to replacing traditional materials like metals and short-fiber composites. Unlike thermosets, LFTs offer the significant advantage of being recyclable and processable using high-speed, efficient methods like compression and direct-injection molding, which is a game-changer for large-scale manufacturing.

Get Full Report Here: https://www.24chemicalresearch.com/reports/264041/global-longfiber-thermoplastics-market-2024-516

Market Dynamics:

The market's growth is propelled by a strong set of drivers, yet it must navigate significant restraints and technical challenges, all while capitalizing on emerging opportunities that promise to reshape its future.

Powerful Market Drivers Propelling Expansion

-

Automotive Industry's Relentless Pursuit of Lightweighting: The automotive sector remains the primary engine of growth for LFTs, driven by stringent global emission regulations. Stricter CO2 targets, such as the EU's goal of a 55% reduction in car emissions by 2030, compel manufacturers to shed vehicle weight. LFT components can be up to 40-50% lighter than equivalent steel parts, directly contributing to a 5-7% improvement in fuel efficiency. The average modern vehicle now incorporates over 30-35 kg of plastic composites, a figure expected to grow significantly with the rise of electric vehicles (EVs), where weight reduction is critical to maximizing battery range.

-

Expansion in Aerospace and Consumer Electronics: Beyond automotive, the aerospace industry is a major adopter, leveraging LFTs for non-critical interior components like seat frames, ducting, and storage bins, achieving weight savings that translate into substantial fuel cost reductions over an aircraft's lifespan. In consumer electronics, the demand for thin, lightweight, yet robust housings for laptops, smartphones, and wearable devices is expanding. LFTs provide the necessary structural integrity and excellent EMI/RFI shielding properties, meeting the dual demands of design aesthetics and functional performance, a market segment growing at over 8% annually.

-

Sustainability and Circular Economy Imperatives: The inherent recyclability of thermoplastics is becoming a powerful market driver. Unlike thermoset composites, which often end up in landfills, LFT components can be granulated and reprocessed multiple times. This aligns perfectly with corporate sustainability goals and evolving regulations around extended producer responsibility (EPR). Major OEMs are increasingly specifying recyclable materials, with LFTs offering a 20-30% lower lifecycle carbon footprint compared to traditional metal alternatives, making them a cornerstone of circular manufacturing strategies.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/264041/global-longfiber-thermoplastics-market-2024-516

Significant Market Restraints Challenging Adoption

Despite the compelling advantages, several factors continue to temper the market's growth trajectory.

-

Higher Raw Material and Processing Costs: The premium performance of LFTs comes at a cost. High-performance polymers like polyamide (PA) and the specialized, continuous fibers used as reinforcement can make raw material costs 30-50% higher than for standard plastics or short-fiber composites. Furthermore, the initial capital investment for specialized processing equipment, such as large-tonnage injection molding machines or compression molding presses with precise temperature controls, poses a significant barrier for small and medium-sized enterprises, limiting wider adoption.

-

Technical Limitations in High-Temperature Applications: While LFTs excel in many areas, their use in under-the-hood automotive applications or aerospace primary structures is limited by thermal performance. Standard polypropylene-based LFTs have heat deflection temperatures typically below 120°C, making them unsuitable for components near engines or exhaust systems. While high-temperature polymers like PEEK-based LFTs exist, their cost is often prohibitive for all but the most critical applications, creating a performance-cost gap that restrains market penetration in certain high-value segments.

Critical Market Challenges Requiring Innovation

The industry faces operational hurdles that demand continuous research and development to overcome.

A primary challenge is achieving consistent fiber length and distribution during processing. Fiber breakage in the plastification unit of injection molding machines can reduce the average fiber length by 30-40%, compromising the very mechanical properties that define LFTs. Optimizing screw design and processing parameters is a constant focus for material suppliers and processors alike. Furthermore, achieving a strong fiber-matrix interface to prevent delamination under cyclic loading is difficult; inadequate adhesion can lead to a 15-20% reduction in predicted fatigue strength, a critical factor for structural components.

Additionally, the market contends with the challenge of design expertise. Successfully integrating LFT components requires a fundamental shift from traditional metal design principles to design for composites. There is a notable shortage of engineers proficient in anisotropic material modeling and simulation, leading to overly conservative designs that fail to fully exploit the material's potential and, paradoxically, increase the part cost per unit of performance.

Vast Market Opportunities on the Horizon

-

Electric Vehicle (EV) Revolution as a Major Catalyst: The unprecedented growth of the electric vehicle market represents the single largest opportunity for LFTs. EVs require extensive lightweighting to offset heavy battery packs, and LFTs are ideal for large, integrated components like battery trays, structural underbody shields, and interior platforms. The global EV battery enclosure market alone is projected to exceed $10 billion by 2028, with LFT composites capturing a significant share due to their combination of light weight, excellent flame retardancy, and mechanical robustness.

-

Advancements in Hybrid and Direct Manufacturing Processes: Innovations in processing technologies are opening new frontiers. The development of the D-LFT (Direct Long-Fiber Thermoplastic) process, where compounding and molding are integrated into a single step, is reducing energy consumption and material waste by 10-15%. Furthermore, hybrid molding techniques, which combine LFT with other materials like metal inserts or overmolded elastomers, are enabling the production of highly complex, multifunctional parts in a single manufacturing cycle, reducing assembly steps and costs.

-

Bio-Based and Sustainable LFT Composites: The push for sustainability is creating a burgeoning market for bio-based LFTs. Developments in polylactic acid (PLA) and polyhydroxyalkanoate (PHA) matrices reinforced with natural fibers like flax or hemp are gaining traction in semi-structural applications in automotive interiors and consumer goods. While currently a niche segment, accounting for less than 5% of the market, it is expected to grow at a rapid pace as bio-polymer performance improves and consumer preference for sustainable products intensifies.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into Polypropylene (PP), Polyamide (PA), Polybutylene Terephthalate (PBT), and others. Polypropylene (PP) currently dominates the market, favored for its excellent balance of properties, ease of processing, and cost-effectiveness, making it the workhorse material for large-volume automotive applications. Polyamide (PA)-based LFTs hold a significant share in applications requiring higher thermal and mechanical performance, albeit at a higher cost.

By Application:

Application segments include Automotive, Aerospace, Electronics, Building & Construction, Sporting Equipment, and others. The Automotive segment is the undisputed leader, consuming over 70% of all LFTs produced. This dominance is driven by the extensive use of LFTs in underbody components, front-end modules, door modules, and interior structures. The Aerospace and Electronics segments are also key growth areas, leveraging the material's specific strength and design flexibility.

By End-User Industry:

The end-user landscape is dominated by the Transportation industry (encompassing automotive, aerospace, and rail). However, the Building & Construction sector is emerging as a promising end-user, particularly for large-profile extruded LFTs used in decking, fencing, and structural profiles where durability and resistance to weathering are paramount.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/264041/global-longfiber-thermoplastics-market-2024-516

Competitive Landscape:

The global Long-Fiber Thermoplastics market is moderately consolidated and characterized by intense competition, technological innovation, and strategic partnerships. The top players—Celanese Corporation, SABIC, and Lanxess AG—collectively command a significant portion of the market share. Their leadership is reinforced by extensive product portfolios, strong technical service capabilities, and global production footprints that allow them to serve multinational OEMs effectively.

List of Key Long-Fiber Thermoplastics Companies Profiled:

-

Celanese Corporation (U.S.)

-

SABIC (Saudi Arabia)

-

Lanxess AG (Germany)

-

Solvay S.A. (Belgium)

-

PolyOne Corporation (Now Avient) (U.S.)

-

PlastiComp Inc. (U.S.)

-

RTP Company (U.S.)

-

Asahi Kasei (Japan)

-

SGL Group (Germany)

-

PPG Fiber Glass Inc. (U.S.)

-

Sumitomo Chemical Company Ltd. (Japan)

-

Technocompound GmbH (Germany)

-

Quadrant AG (Switzerland)

-

Kingfa (China)

-

Daicel Polymer Limited (Japan)

-

Dieffenbacher (Germany)

The prevailing competitive strategy focuses heavily on developing new high-performance resin systems, optimizing manufacturing processes to reduce costs, and forming deep, collaborative partnerships with OEMs to design and certify components for next-generation vehicles and products.

Regional Analysis: A Global Footprint with Distinct Leaders

-

Asia-Pacific: Is the dominant force in the global LFT market, accounting for over 45% of consumption. This leadership is anchored by China, the world's largest automotive producer, and supported by a massive manufacturing base, strong government support for advanced materials, and growing domestic demand. Japan and South Korea are also major contributors, driven by their technologically advanced automotive and electronics industries.

-

Europe & North America: Together, they form the other major bloc, with Europe holding a slightly larger share due to its strong automotive OEM presence and stringent environmental regulations that drive lightweighting. North America's market is robust, fueled by a resurgence in automotive manufacturing and significant adoption in the aerospace and consumer goods sectors. Both regions are characterized by high levels of innovation and a focus on premium, high-performance LFT applications.

-

Rest of the World (South America, MEA): These regions represent emerging markets with significant growth potential. While currently smaller, increasing industrialization, investments in infrastructure, and the gradual establishment of local automotive production are expected to drive future demand for LFTs.

Get Full Report Here: https://www.24chemicalresearch.com/reports/264041/global-longfiber-thermoplastics-market-2024-516

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/264041/global-longfiber-thermoplastics-market-2024-516

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

-

Plant-level capacity tracking

-

Real-time price monitoring

-

Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/