Agricultural Fumigants Market: A Comprehensive Overview of Growth, Trends, and Opportunities

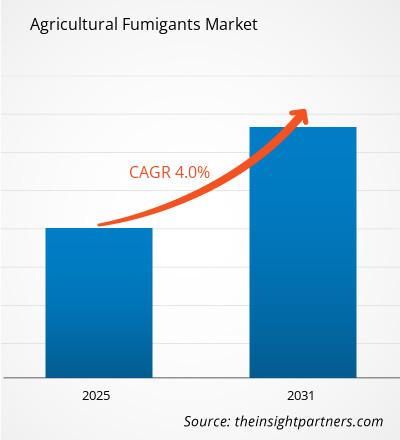

The global Agricultural Fumigants Market is emerging as a critical segment within the agrochemical industry, driven by the world's urgent need to secure food production and manage pest threats more effectively. According to a detailed market research report by The Insight Partners, the agricultural fumigants market is set to register a compound annual growth rate (CAGR) of 4% between 2025 and 2031, signaling steady and sustained expansion over the coming years. With historical data spanning from 2021 to 2023 and a base year set at 2024, the report offers a thorough lens through which stakeholders can evaluate both current dynamics and future trajectories.

What Are Agricultural Fumigants?

Agricultural fumigants are chemical substances used to eliminate pests, insects, fungi, and other harmful organisms in soils and stored grain facilities. They are deployed in various forms — solid, liquid, and gas — and applied across a range of agricultural settings, from open farmland to warehouse storage units. Key product types covered in the market analysis include methyl bromide, phosphine, chloropicrin, metam sodium, and 1,3-dichloropropene, each offering distinct advantages depending on the pest profile and application environment.

Access Report for More Info: https://www.theinsightpartners.com/reports/agricultural-fumigants-market

Key Market Drivers

Several powerful forces are fuelling the growth of the agricultural fumigants market. The most significant among them is the rising global population, which continues to place immense pressure on agricultural systems to produce more food with fewer losses. Farmers worldwide are increasingly turning to fumigants as a reliable tool for eliminating pests and diseases that would otherwise reduce crop yields. Beyond population growth, regulatory support in many countries is actively encouraging the adoption of safer fumigation practices, with governments enacting policies that balance effective pest control with environmental responsibility. Additionally, the growing emphasis on food safety across global supply chains is boosting demand for fumigants that help keep stored grains and produce pest-free, ensuring quality from farm to table.

Regional Insights

From a geographical standpoint, Asia Pacific currently dominates the global agricultural fumigants market. This leadership is attributed to the region's rapidly expanding agricultural industry, a surging population base, and increasing levels of agricultural production. Countries like China, India, and Japan are key contributors to this regional share. Meanwhile, North America and Europe represent mature but steady markets, with ongoing innovation and regulatory frameworks shaping consumption patterns. Emerging markets in South and Central America as well as the Middle East and Africa present exciting growth opportunities, particularly as climate change intensifies the need for robust pest management solutions across these regions.

Future Trends Shaping the Industry

Looking ahead, the market is poised to undergo significant transformation. One of the most prominent trends is the industry-wide shift toward biodegradable and environmentally safe fumigants. As governments tighten regulations and public awareness around environmental sustainability grows, the demand for less toxic alternatives is expected to rise sharply. Smart farming technologies are also entering the picture, with the integration of IoT, GPS, and data analytics enabling farmers to apply fumigants more precisely, reducing waste and improving overall pest management efficiency. The expansion of the biopesticides market further signals a broader restructuring of how the agricultural sector approaches pest control.

Key Players

The agricultural fumigants market is home to several industry titans. Major players include ADAMA Ltd., AMVAC Chemical Corporation, Arkema Group, BASF SE, Isagro SpA, LANXESS AG, Nippon Chemical Industrial Co., Solvay SA, and Syngenta AG. These companies are actively investing in research, innovation, and strategic partnerships to maintain their competitive edge in an evolving marketplace.

Conclusion

The agricultural fumigants market stands at an inflection point — balancing the immediate need for effective pest control with the long-term imperative of environmental and health sustainability. With a projected 4% CAGR through 2031 and a growing emphasis on safer, smarter farming technologies, the market offers compelling opportunities for manufacturers, investors, and policymakers alike. As the industry continues to innovate, agricultural fumigants will remain a cornerstone of global food security strategies for years to come.

The global Agricultural Fumigants Market is emerging as a critical segment within the agrochemical industry, driven by the world's urgent need to secure food production and manage pest threats more effectively. According to a detailed market research report by The Insight Partners, the agricultural fumigants market is set to register a compound annual growth rate (CAGR) of 4% between 2025 and 2031, signaling steady and sustained expansion over the coming years. With historical data spanning from 2021 to 2023 and a base year set at 2024, the report offers a thorough lens through which stakeholders can evaluate both current dynamics and future trajectories.

What Are Agricultural Fumigants?

Agricultural fumigants are chemical substances used to eliminate pests, insects, fungi, and other harmful organisms in soils and stored grain facilities. They are deployed in various forms — solid, liquid, and gas — and applied across a range of agricultural settings, from open farmland to warehouse storage units. Key product types covered in the market analysis include methyl bromide, phosphine, chloropicrin, metam sodium, and 1,3-dichloropropene, each offering distinct advantages depending on the pest profile and application environment.

Access Report for More Info: https://www.theinsightpartners.com/reports/agricultural-fumigants-market

Key Market Drivers

Several powerful forces are fuelling the growth of the agricultural fumigants market. The most significant among them is the rising global population, which continues to place immense pressure on agricultural systems to produce more food with fewer losses. Farmers worldwide are increasingly turning to fumigants as a reliable tool for eliminating pests and diseases that would otherwise reduce crop yields. Beyond population growth, regulatory support in many countries is actively encouraging the adoption of safer fumigation practices, with governments enacting policies that balance effective pest control with environmental responsibility. Additionally, the growing emphasis on food safety across global supply chains is boosting demand for fumigants that help keep stored grains and produce pest-free, ensuring quality from farm to table.

Regional Insights

From a geographical standpoint, Asia Pacific currently dominates the global agricultural fumigants market. This leadership is attributed to the region's rapidly expanding agricultural industry, a surging population base, and increasing levels of agricultural production. Countries like China, India, and Japan are key contributors to this regional share. Meanwhile, North America and Europe represent mature but steady markets, with ongoing innovation and regulatory frameworks shaping consumption patterns. Emerging markets in South and Central America as well as the Middle East and Africa present exciting growth opportunities, particularly as climate change intensifies the need for robust pest management solutions across these regions.

Future Trends Shaping the Industry

Looking ahead, the market is poised to undergo significant transformation. One of the most prominent trends is the industry-wide shift toward biodegradable and environmentally safe fumigants. As governments tighten regulations and public awareness around environmental sustainability grows, the demand for less toxic alternatives is expected to rise sharply. Smart farming technologies are also entering the picture, with the integration of IoT, GPS, and data analytics enabling farmers to apply fumigants more precisely, reducing waste and improving overall pest management efficiency. The expansion of the biopesticides market further signals a broader restructuring of how the agricultural sector approaches pest control.

Key Players

The agricultural fumigants market is home to several industry titans. Major players include ADAMA Ltd., AMVAC Chemical Corporation, Arkema Group, BASF SE, Isagro SpA, LANXESS AG, Nippon Chemical Industrial Co., Solvay SA, and Syngenta AG. These companies are actively investing in research, innovation, and strategic partnerships to maintain their competitive edge in an evolving marketplace.

Conclusion

The agricultural fumigants market stands at an inflection point — balancing the immediate need for effective pest control with the long-term imperative of environmental and health sustainability. With a projected 4% CAGR through 2031 and a growing emphasis on safer, smarter farming technologies, the market offers compelling opportunities for manufacturers, investors, and policymakers alike. As the industry continues to innovate, agricultural fumigants will remain a cornerstone of global food security strategies for years to come.

Agricultural Fumigants Market: A Comprehensive Overview of Growth, Trends, and Opportunities

The global Agricultural Fumigants Market is emerging as a critical segment within the agrochemical industry, driven by the world's urgent need to secure food production and manage pest threats more effectively. According to a detailed market research report by The Insight Partners, the agricultural fumigants market is set to register a compound annual growth rate (CAGR) of 4% between 2025 and 2031, signaling steady and sustained expansion over the coming years. With historical data spanning from 2021 to 2023 and a base year set at 2024, the report offers a thorough lens through which stakeholders can evaluate both current dynamics and future trajectories.

What Are Agricultural Fumigants?

Agricultural fumigants are chemical substances used to eliminate pests, insects, fungi, and other harmful organisms in soils and stored grain facilities. They are deployed in various forms — solid, liquid, and gas — and applied across a range of agricultural settings, from open farmland to warehouse storage units. Key product types covered in the market analysis include methyl bromide, phosphine, chloropicrin, metam sodium, and 1,3-dichloropropene, each offering distinct advantages depending on the pest profile and application environment.

👉 Access Report for More Info: https://www.theinsightpartners.com/reports/agricultural-fumigants-market

Key Market Drivers

Several powerful forces are fuelling the growth of the agricultural fumigants market. The most significant among them is the rising global population, which continues to place immense pressure on agricultural systems to produce more food with fewer losses. Farmers worldwide are increasingly turning to fumigants as a reliable tool for eliminating pests and diseases that would otherwise reduce crop yields. Beyond population growth, regulatory support in many countries is actively encouraging the adoption of safer fumigation practices, with governments enacting policies that balance effective pest control with environmental responsibility. Additionally, the growing emphasis on food safety across global supply chains is boosting demand for fumigants that help keep stored grains and produce pest-free, ensuring quality from farm to table.

Regional Insights

From a geographical standpoint, Asia Pacific currently dominates the global agricultural fumigants market. This leadership is attributed to the region's rapidly expanding agricultural industry, a surging population base, and increasing levels of agricultural production. Countries like China, India, and Japan are key contributors to this regional share. Meanwhile, North America and Europe represent mature but steady markets, with ongoing innovation and regulatory frameworks shaping consumption patterns. Emerging markets in South and Central America as well as the Middle East and Africa present exciting growth opportunities, particularly as climate change intensifies the need for robust pest management solutions across these regions.

Future Trends Shaping the Industry

Looking ahead, the market is poised to undergo significant transformation. One of the most prominent trends is the industry-wide shift toward biodegradable and environmentally safe fumigants. As governments tighten regulations and public awareness around environmental sustainability grows, the demand for less toxic alternatives is expected to rise sharply. Smart farming technologies are also entering the picture, with the integration of IoT, GPS, and data analytics enabling farmers to apply fumigants more precisely, reducing waste and improving overall pest management efficiency. The expansion of the biopesticides market further signals a broader restructuring of how the agricultural sector approaches pest control.

Key Players

The agricultural fumigants market is home to several industry titans. Major players include ADAMA Ltd., AMVAC Chemical Corporation, Arkema Group, BASF SE, Isagro SpA, LANXESS AG, Nippon Chemical Industrial Co., Solvay SA, and Syngenta AG. These companies are actively investing in research, innovation, and strategic partnerships to maintain their competitive edge in an evolving marketplace.

Conclusion

The agricultural fumigants market stands at an inflection point — balancing the immediate need for effective pest control with the long-term imperative of environmental and health sustainability. With a projected 4% CAGR through 2031 and a growing emphasis on safer, smarter farming technologies, the market offers compelling opportunities for manufacturers, investors, and policymakers alike. As the industry continues to innovate, agricultural fumigants will remain a cornerstone of global food security strategies for years to come.

0 Commenti

0 condivisioni

235 Views